| Article Section | |||||||||||

ROI- due date in case of partner of firm liable to tax audit S.139 – words ‘ a partner’ need to be substituted in place of ‘a working partner’ in provisions , meanwhile a circular is desirable |

|||||||||||

|

|||||||||||

ROI- due date in case of partner of firm liable to tax audit S.139 – words ‘ a partner’ need to be substituted in place of ‘a working partner’ in provisions , meanwhile a circular is desirable |

|||||||||||

|

|||||||||||

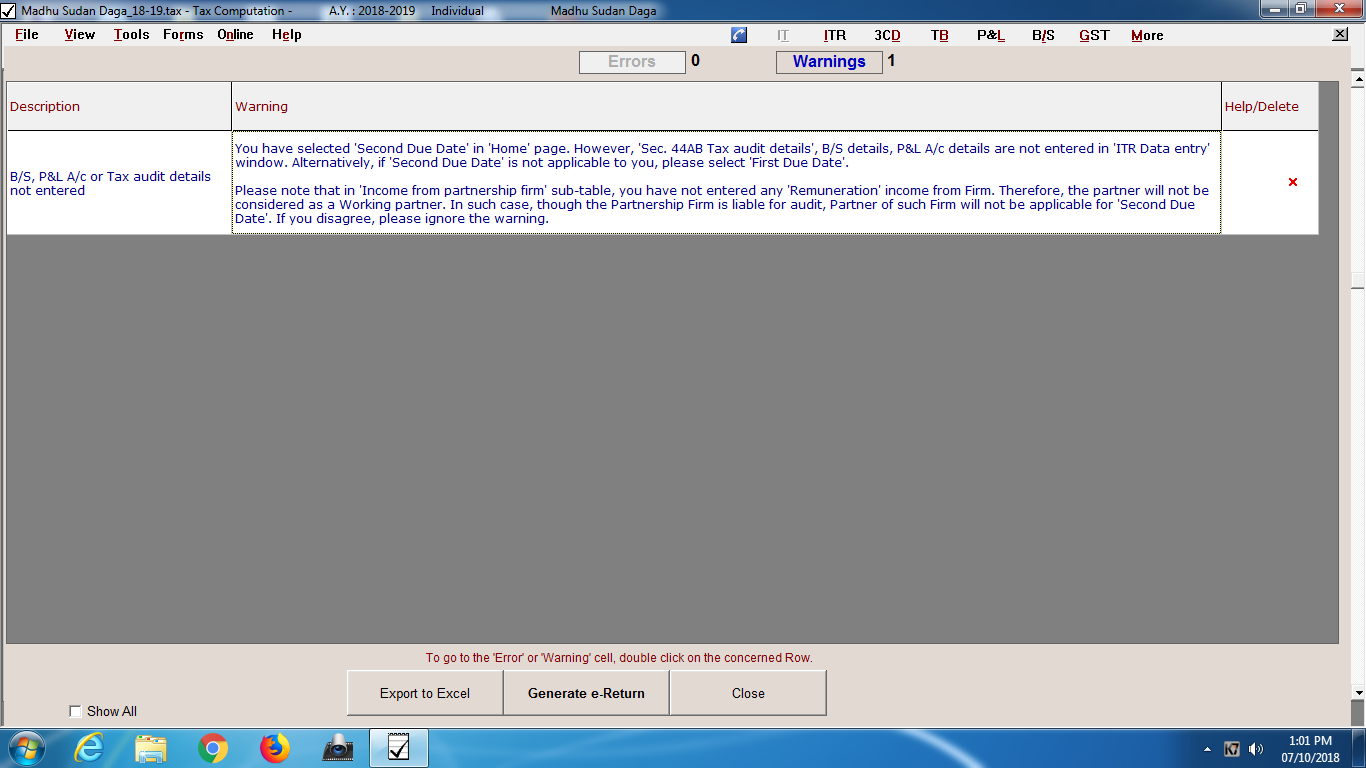

Section 139 of Income-tax Act ,1961.(ITA) Orders extending date of filing of ROI from time to time. Due date for filing of Return of income (ROI): Provision of S.139 of ITA prescribes due date for filing of ROI (and Return of Loss). For the purpose of this write-up we are concerned with S.139(1) which provides due date for filing of Return. Other provisions deal with some other situations for filing of ROI or RO Loss, Revised Return etc. Due date as prescribed in S.139.1 is relevant for the purpose for levy of interest u/s 134A , some deductions allowable , carry forward of loss . Extension of due date: Many times due to certain reasons due date u/s 139.1 is revised by the CBDT so as to overcome difficulties of the persons required to file ROI. For example, currently we are concerned with due date of filing of ROI by person who are liable to get their accounts audited u/s 44AB ( Tax Audit Report- TAR) As is well known by readers such revised / extended date is 15.10.2018. Such date is described ‘second due date in ITR software utility. Partners of firms required to get TAR: In case of partners of firms which are required to get TAR, finalisation of account and obtaining TAR is important even for the purpose of computation of income of partner. A partner may derive income from firm in which he is partner in several ways. Popular method of distribution of profits of firm amongst partners are as follows: a. Interest on capital of partners infirm, b. Interest on current account of partners in firm, c. Remuneration of partners, d. Commission or other rewards to partners, e. Share in profit of the firm. Items a. to d. and similar other expenses of firm are allowable to firm (subject to some conditions), and these are taxable in hands of partners. Item e. is application of income of firm and is not allowable to the firm , frim pays tax on profits of firm, and as a consequence partner get his share in profit as exempt income. Dependence of amount of above items in books of firm: Amount of above items are dependent terms and conditions in partnership deed and also on finalisation of accounts of the firm. Interest may be higher or lesser depending on amount of profit or variation in terms and conditions, overall remuneration which firm can pay (and will be allowable) also depend on amount of profit. The amount of profit of firm and share in profit of firm of each of its partners is the last item, which can be determined only after computing profit of firm after interest to partners, remuneration of partners shall depend on profit after interest, share in profit will be on the basis of profit after all chargeable items including remuneration to partners. Taxable profit of firm will depend on amount allowable on account of payments made to partners besides normal computation. Remuneration to partners: Remuneration to partners may or may not be payable, it depends on terms and conditions in partnership deed (which can also be revised from time to time). It is not necessary that each and every partner is paid some remuneration from the firm. In many cases no remuneration is paid to partners/ senior partners). In case of professional firms senior partners may not take remuneration and remuneration may be paid only to junior partners. This does not means that a partner who has not been paid remuneration is not a working partner. A partner can work and not get remuneration, instead he may prefer to receive share in profit. In many cases of family members controlled firms or firms of friend’s remuneration and interest on capital may not be paid. Instead partners prefer to get share in profit and no other rewards from the firm. This may be due to simplicity when there is no interest and remuneration paid to partners. Therefore, when remuneration is not paid by firm and no remuneration is claimed and received by any partners does not mean that the partner not receiving remuneration is not a working partner of the firm. Due date in case of partners of firm required to obtain TAR: Relevant portion of S.139.1 is reproduced below: Return of income. 139. 1[(1) Every person,- (a) being a company 2[or a firm]; or (b) being a person other than a company 3[or a firm], if his total income or the total income of any other person in respect of which he is assessable under this Act during the previous year exceeded the maximum amount which is not chargeable to income-tax, shall, on or before the due date, furnish a return of his income or the income of such other person during the previous year, in the prescribed form and verified in the prescribed manner and setting forth such other particulars as may be prescribed : Provided also that every company 7[or a firm] shall furnish on or before the due date the return in respect of its income or loss in every previous year : Explanation 2.-In this sub-section, "due date" means,- (a) where the assessee 65[other than an assessee referred to in clause (aa)] is- (i) a company 60[******]; or (ii) a person (other than a company) whose accounts are required to be audited under this Act or under any other law for the time being in force; or (iii) a working partner of a firm whose accounts are required to be audited under this Act or under any other law for the time being in force, the 58[30th day of September] of the assessment year; From reading of the provisions, we find that a firm is required to file Return of Income even if it has no taxable income. In case firm is required to obtain TAR then the due date is 30th September of the assessment year for such firm. The provision for due date in relation to a working partner of such firms who are required to get TAR is also the same as is in case of firm. As discussed earlier, it is desirable that the due date as in case of firm should also be due date for any partner. Words ‘a working partner’ should be substituted by words ‘a partner’ in the clause of the Explanation referred above. Merely because a partner has not received remuneration should not be a reason to determine due date in case of partner which is prior to due date in case of the firm. Working partner: Generally all individual partners in a firm are working partners unless it is specifically provided that a particular partner will not be working partner or will be a totally sleeping partner. Even in case of partners being HUF or company, partner can be working partner as Karta of HUF or any other member of HUF and any officer of company can work for the firm in interest of firm and also for safeguard of the partner ( HUF or company as the case may be). No remuneration does not mean that partner is not working partner: As discussed earlier the fact that no remuneration is received by partner from the firm does not mean that the partner is not a working partner. Even in case of HUF or company partners, such partners are working partner as representative/ nominees of HUF or company work for the firm on behalf of such partners. Even otherwise return of partner is dependent on ROI of firm: As discussed earlier, even for ascertaining various type of income of partners it is necessary that the accounts of the firm should be finalised. Therefore, due date in case of partner of any firm should be due date applicable in case of the firm. Amendment in S. 139 is desirable: As discussed earlier, it is desirable that the due date as in case of firm should also be due date for any partner. Words ‘a working partner’ should be substituted by words ‘a partner’ in the clause of the Explanation referred above. Merely because a partner has not received remuneration should not be a reason to determine due date in case of partner which is prior to due date in case of the firm. Error/ warning message appearing at the time of filing of ROI of partner: When a ROI of partner is being filed, in case there is no remuneration received, the ROI utility software is generating and displaying the following message:

From above message it seems that in software utility, it is presumed that in case a partner has not received remuneration from firm, he is not a working partner. This is wrong presumption as discussed in this article. A partner not only individual but also a HUF and a company can be working partner. The expression ‘working partner’ has to be understood in accordance with commercial aspects and ground realities. Even otherwise, it will not be possible for a partner to file correctly his ROI before he gets final accounts of firm In such cases the partner may choose to ignore the warning. Circular and amendment in ITR utility is desirable: To remove difficulties of partners of firms, a circular from the CBDT and changes in ITR utility software etc. are desirable so that the second due date is accepted (without error message and objection) in case of partner, even f remuneration is not received from firm. --------- CA Dev Kumar Kothari and CA Rajendra Kumar Rathi

By: CA DEV KUMAR KOTHARI - October 10, 2018

|

|||||||||||

| |

|||||||||||