Taxation of ULIP - In case of ULIP, When the premium payable for ...

Income Tax

June 2, 2023

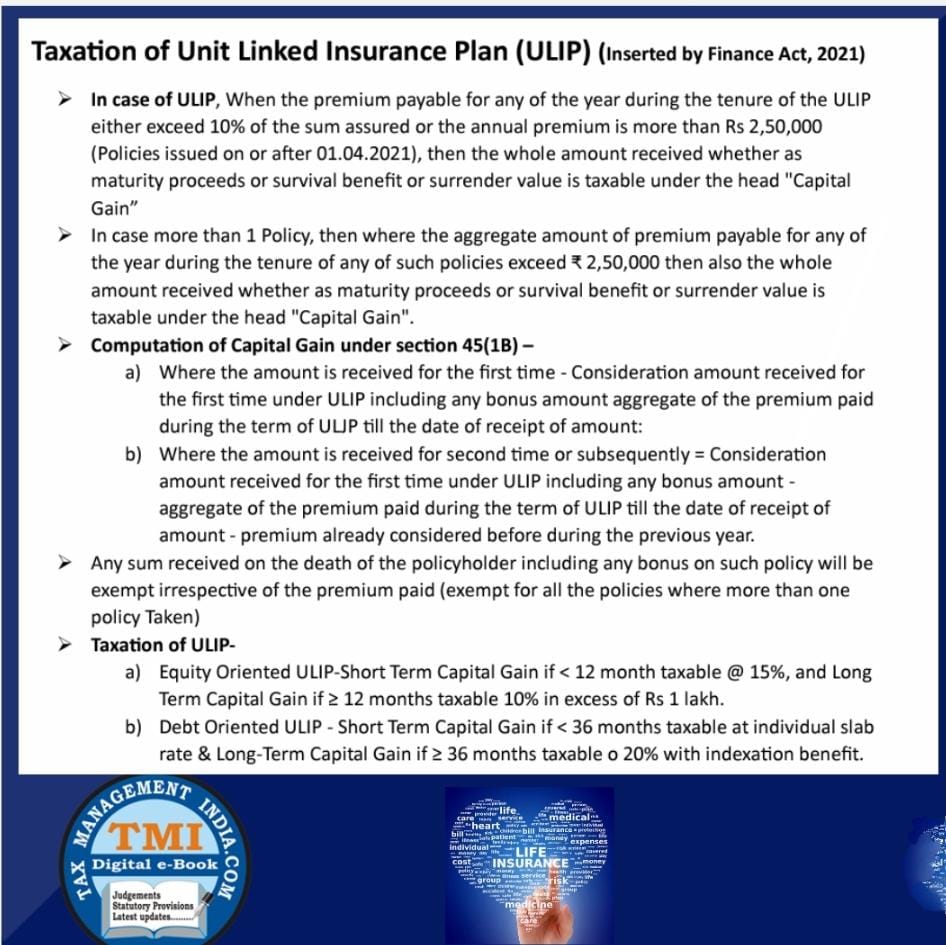

Taxation of ULIP - In case of ULIP, When the premium payable for any of the year during the tenure of the ULIP either exceed 10% of the sum assured or the annual premium is more than Rs 2,50,000 (Policies issued on or after 01.04.2021), then the whole amount received whether as maturity proceeds or survival benefit or surrender value is taxable under the head "Capital Gain” Sec 45(1B) r.w.r. 8AD

View Source