| Article Section | ||||||||||||

|

Home |

||||||||||||

New Insight for Renting of a Motor Vehicle under GST on RCM |

||||||||||||

|

||||||||||||

New Insight for Renting of a Motor Vehicle under GST on RCM |

||||||||||||

|

||||||||||||

The activity “Renting of a Motor Vehicle”has been brought under RCM during September 2019 with a limited compliance requirement under Section 9(3) of CGST Act, 2017. However, Government authorities felt that the compliance requirement under the above entry has been unclear in Trade & Industry, where by they have issued a Circular No.130/2019 dtd:31.12.2019. There is a scope for the Registered person to understand the compliance requirement in this regard and to augment cost reduction by way of tax planning at the Service provider end. We shall examine this in detail from the following paragraphs, only after if we perceive the intended meaning of the proposed entry in this regard: Original Entry Notification 22/2019 dtd:30.09.2019:

New version for the activity of “Renting of a Motor Vehicle” under RCM w.e.f. 31.12.2019 vide Notification No.29/2019 CTR dtd:31.12.2019 inserted for the above entry as below:

Currently there are two category of services which requires more explicitness from the Government authorities for its existence and also under what circumstances those services become mutually exclusive for their operation. First category is “Passenger Transportation service – SAC 9964” and second category is “Renting service of motor vehicles with operator – SAC 9966”. In general all the Body Corporate have an intent of providing transport facility to their employees from a standard point of alight to the factory and back to such place of origin. Renting of a motor vehicle and passenger transportation have some sort of similarity for their existence Points to note for compliance in this regard:

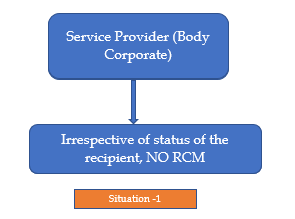

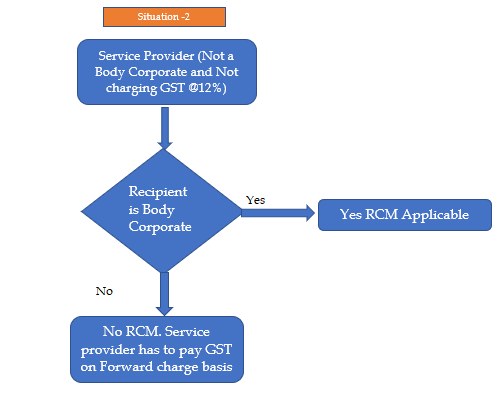

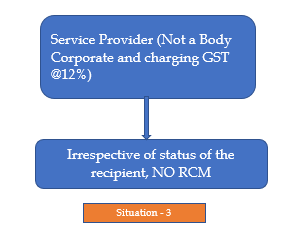

We shall summarise the applicability of GST on Forward / Reverse charge basis as per below flow charts:

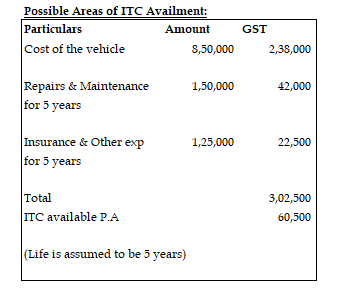

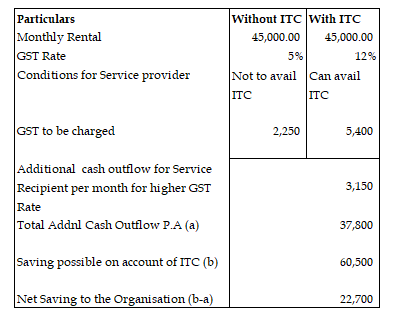

Now we shall examine the tax planning to be made at the Service provider end who is Registered under GST to adopt for charging GST @12% by availing Input Tax credit. An illustration has been made for ease of understanding on some hypothetical circumstances as below:

Comments:

The above Notification has been issued on 31.12.2019 widening the scope and ambit of coverage for the circumstances under which tax needs to be paid on RCM basis. Accordingly, all the bills received for Dec’19 and thereafter we need to pay GST on RCM basis. Though the Circular No.130/2019 issued at para 6 has clarified that the insertion made in Notification 29/2019 dtd: 31.12.2019 is effective from 01.10.2019, we understand that an amendment made to the levy provision has to be prospective and cannot be retrospective in nature

By: Gella Praveenkumar - January 8, 2020

|

||||||||||||

| |

||||||||||||