| Article Section | |||||||||||

|

Home |

|||||||||||

CAROTAR 2020- Bonus or Burdensome for Importers |

|||||||||||

|

|||||||||||

CAROTAR 2020- Bonus or Burdensome for Importers |

|||||||||||

|

|||||||||||

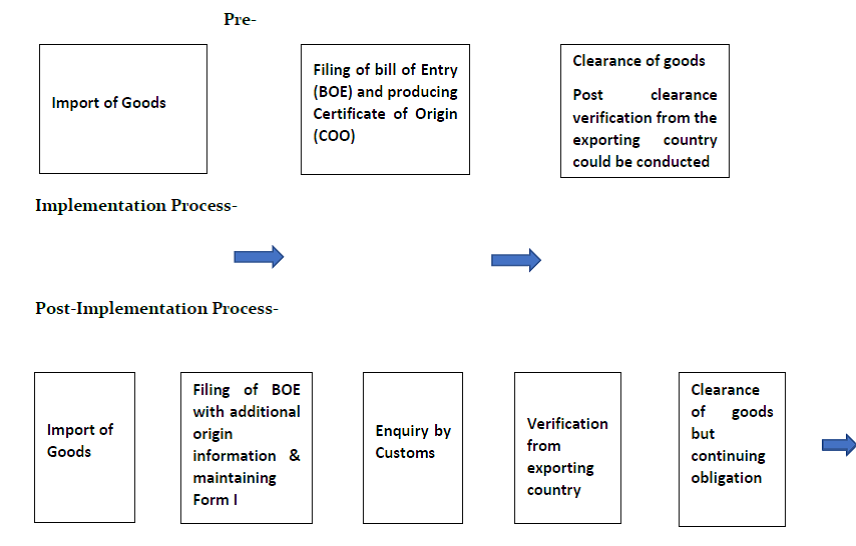

CAROTAR 2020-Availment of Preferential rate of duty A. What is CAROTAR The Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020 (CAROTAR, 2020), was notified on 21st August 2020 by the Central Board of Indirect Taxes and Customs. It came into force with effect from 21 September 2020. It was introduced for administering the verification of the country of origin of the goods imported under preferential tariff FTAs with different countries. B. Comparison between Pre and Post implementation of CAROTAR 2020

* Increase in information requirement to substantiate the origin **Increased dependence on global suppliers for real time information C. Additional Information required on Bill of Entry

D. Possession of requisite information before Import of Goods Primary Information-

In case of Wholly Obtained Goods Process through which goods claimed to be wholly obtained along with backup documentation

In case of Not Wholly Obtained Goods

Author Comments Taxpayers should evaluate the countries from which preferential rate of duty is being claimed under trade agreements. Depending upon whether the imported items are wholly obtained or not wholly obtained, Company must possess the requisite information at the time of importation of goods. Further, the questionnaire is required to be prepared in respect of each SKU in advance along with the backup documentation as per Form I. In case the importer fails to provide the requisite information for any reason, a proper officer can cause further verification consistent with the relevant trade agreement or its rules of origin. In the event of a conflict between a provision of CAROTA rules and a provision of the Rules of Origin, the provision of the Rules of Origin shall prevail to the extent of the conflict. Thus, the company needs to ensure that the proper originating criteria are being met while claiming the benefit of the free trade agreement.

By: Kapil Mahani - September 23, 2022

|

|||||||||||

| |

|||||||||||