| Article Section | |||||||||||

|

Home |

|||||||||||

GSTR 1A return shows the amendments, modifications or deletions made by the recipient in GSTR 2 return. In this article, we look at details to be provided in GSTR 1A return in detail. |

|||||||||||

|

|||||||||||

GSTR 1A return shows the amendments, modifications or deletions made by the recipient in GSTR 2 return. In this article, we look at details to be provided in GSTR 1A return in detail. |

|||||||||||

|

|||||||||||

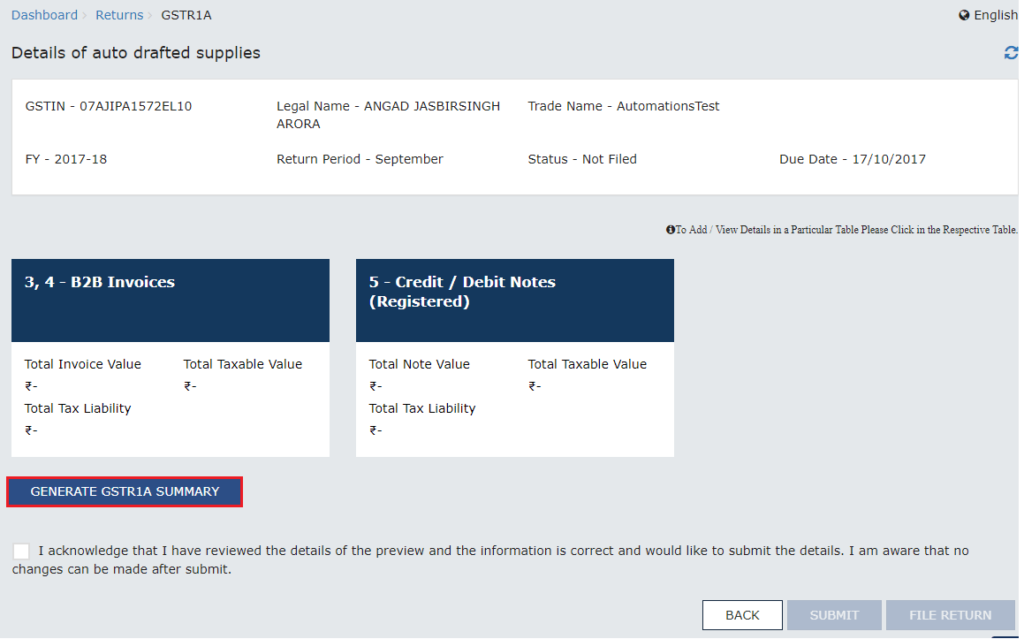

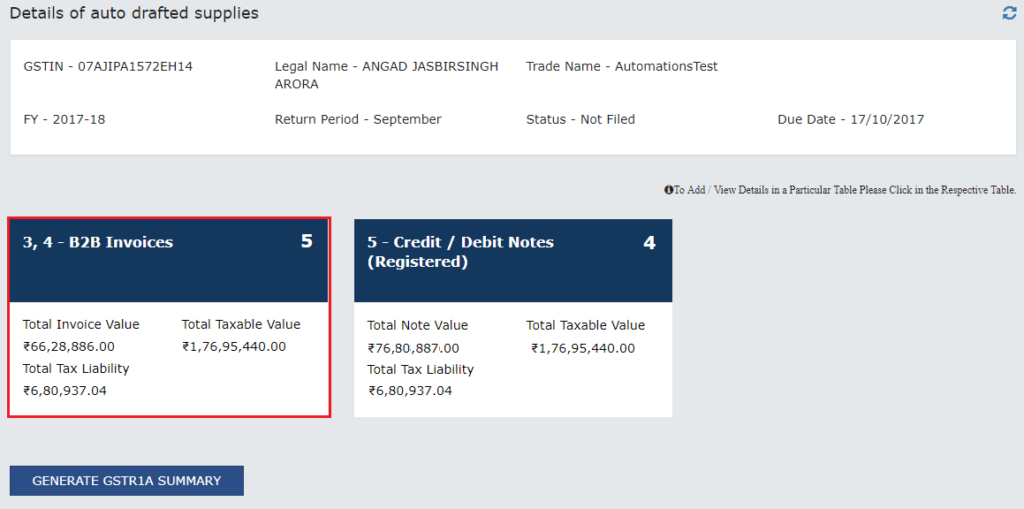

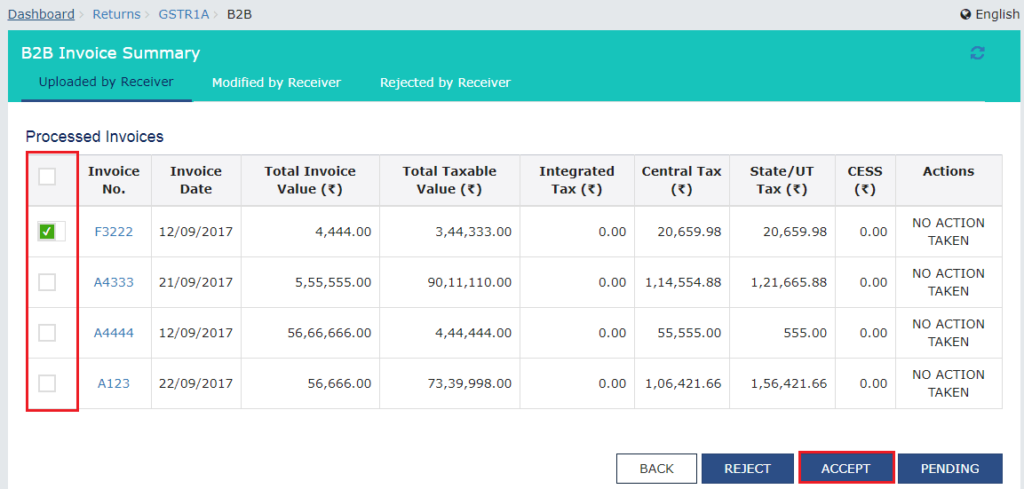

All about GSTR -1A Introduction: GSTR 1A return shows the amendments, modifications or deletions made by the recipient in GSTR 2 return. In this article, we look at details to be provided in GSTR 1A return in detail. GSTR-1A is an addendum to GSTR-1- Outward supplies statement of the supplier. It is always generated on the basis of details added/ modified/ deleted by the counterparty (B2B Transactions) in GSTR- 2/4/6. The details so created in the system are then auto-populated to the supplier on submission of GSTR- 2/4/6. GSTR-1A is generated after the end of tax period and only if the supplier has filed his GSTR-1 before the receiver files his GSTR-2/4/6. All normal taxpayers and casual taxpayers are required to file GSTR-1A. GSTR-1A can be filed from the returns section of the GST Portal. In the post login mode, you can access it by going to Services > Returns > Returns Dashboard. After selecting the financial year and tax period, GSTR-1A in the given period will be displayed. Supplier can file GSTR-1A only from 16th till 17th of the month succeeding the tax period. (For July date is 6TH December). Supplier can take actions (including filing) in GSTR-1A only from 16th till 17th of the month succeeding the tax period. GSTR-1A can be filed before filing of GSTR-2. GSTR-1A is generated when the recipient in GSTR-2/4/6 takes any of the following action:

All the above details get auto-populated to the supplier in the Form GSTR- 1A only if the following conditions are met:

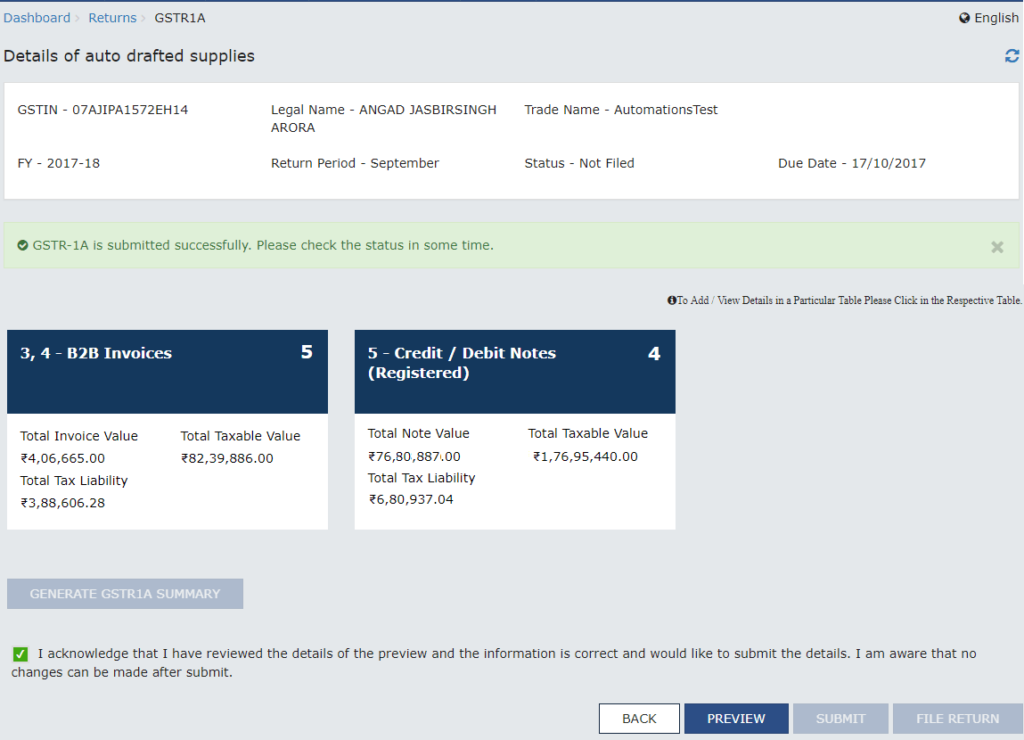

If any one of the above mentioned conditions are met, then all such modifications/ additions/ rejections will flow to the suppliers’ GSTR-1 of the subsequent tax period. Supplier cannot add any details in GSTR-1A. GSTR-1A is not mandatory to be submitted before generation of GSTR-3. In a case where GSTR-1 has not been filed for M tax period before GSTR- 2/4/6, the details added by the counter party are auto populated to GSTR-1 of the M tax period of the supplier who may include the same for submitting his GSTR-1. In case, GSTR-1A has been generated by the taxpayer and not submitted and in the meantime some receivers have filed GSTR- 2/4/6, then the supplier has to generate GSTR-1A again before submission. However, details on which supplier has already taken action will not be impacted due to regeneration of GSTR-1A. If GSTR-1A has been submitted, then all the details which have been kept pending by taxpayer will roll over to GSTR-1 of next tax period. Post 17th of succeeding month of tax period, if GSTR-3 has not been filed, taxpayer will be able to see the GSTR-1A, however, he won’t be allowed to take any actions on the same. If GSTR-1A has not been filed by taxpayer till 17th of the subsequent month of the tax period, then on generation of GSTR-3 by taxpayer, all the details will roll over to GSTR-1 of next tax period. In case of non-filing of GSTR-1A, roll over of details will happen on generation of GSTR-3, whether GSTR-3 has been filed after 17th or before 17th. Post 17th of succeeding month of tax period, if GSTR-3 has not been filed, taxpayer will be able to see the GSTR-1A, however, he won’t be allowed to take any actions on the same. How to file GSTR 1A Return On GST Portal ? Step 1: Login to GST Portal and Select GSTR 1A Step 3: View B2B Invoices Summary

Step 5: File GSTR 1A Return

The author is a practising CA based in Delhi and is registered Insolvency Professional. He can be reached at [email protected] , Mob. +91 9953587496.

By: CA.VINOD CHAURASIA - November 13, 2017

|

|||||||||||

| |

|||||||||||