| Article Section | |||||||||||

Details and information in e-proceedings need to be more relevant and timely to make e-proceeding user friendly. |

|||||||||||

|

|||||||||||

Details and information in e-proceedings need to be more relevant and timely to make e-proceeding user friendly. |

|||||||||||

|

|||||||||||

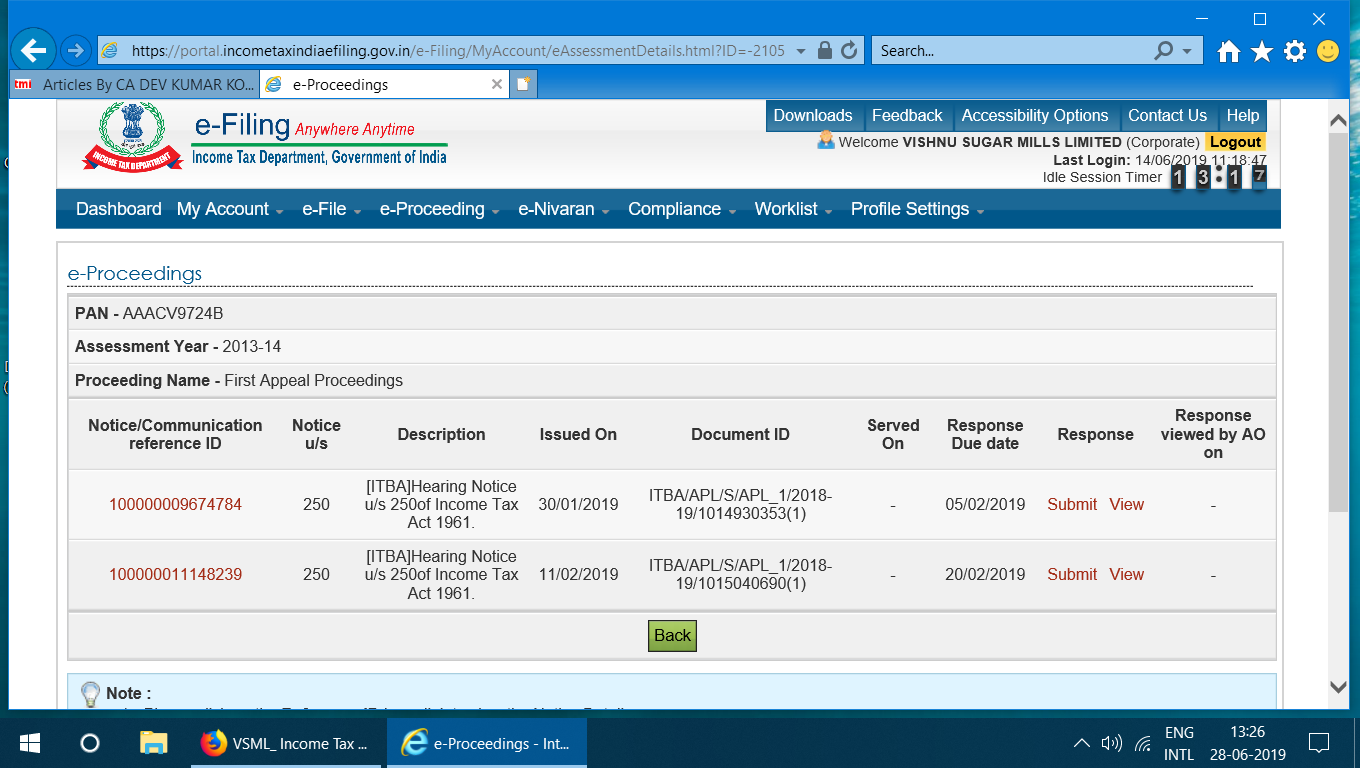

Websites of income tax department (ITD): Websites of ITD are well designed and are user friendly. We find some improvements in the websites from time to time. Feedback sent are also acted upon and implemented. However there is always scope of improvement. One of website of ITD is https://www.incometaxindiaefiling.gov.in Through this website e-filing takes place and assesse can access the website through my account feature after registration. Various information and documents filed, notices issued orders passed etc. can be viewed and downloaded. Requests can be made. e-proceedings: Under link e-proceedings one can look into e-proceedings initiated against assesse like for intimation and assessment of e- returns filed, appeals e- filed etc. There should be also reflection about action of concerned authority. This can include response viewed by concerned authority, order passed etc. It appears that such information are not updated and there is lacking from the officers in placing information available to assesse through my account. For example in case of appeals pending in e-proceedings, assesse can respond to notices issued for hearing and file relevant documents. There should be response by the CIT(A) and information should be updated about further steps taken by CIT(A) and whether he has viewed responses submitted by assesse / appellant. Whether , order has been passed or not. In some cases it is experienced that appeal was in e-proceedings, assesse opted for e-proceeding ( which is by default. Assesse furnished written submissions and paper book. However, CIT(A) passed order dismissing appeal statin that there was no compliance. The appeal could have been decided even based on statement of facts and grounds of appeal because the order passed by AO was contrary to binding judgments and all facts were incorporated in appeal memo. In e-proceeding also detailed submission were available. However, CIT(A) for reasons best known to him only dismissed appeal alleging that the appellant has not attended hearing and has not filed written submission. Perhaps this was the simplest way in which CIT(A) dismissed appeal and confirmed demand. Perhaps in hope of some rewards from department for quick disposal and confirming demand. Wrong or defective system: In case of appeals we also find that there is column ‘response viewed by AO on’. The question is , why AO should view response filed by appellant before CIT(A). The question is why there should not be information about ‘Response viewed by CIT(A). This may be a typographical mistake whereby AO is typed in columns and it should be CIT(A) or concerned authority. For example see the following screen shot about an appeal before CIT(A), in which case responses were filed by appellant / assessee on 05.02.2019 and 20.02.2019. After last submission on 20.02.2019 more than four months have lapsed. There is no information about whether CIT(A) or AO or concerned authority.

In view of above appellant is in dark about fate of appeal and responses filed four months ago. Appellant will be shocked, if one day in a shocking surprise an order will be received that appeal is dismissed for non-prosecution, as happened in some other cases in which CIT(A) ignored submissions made in e-proceedings when e-proceeding was open and a date was fixed for submissions and appellant had in fact made submission online through the link in e-proceeding which was totally ignored by CIT(A)- may be as a handy tool to harass the appellant. The above referred cases are just few examples, there is need to regularly review all web pages and make improvement by ensuring timely, accurate and relevant information.

By: DEVKUMAR KOTHARI - July 2, 2019

|

|||||||||||

| |

|||||||||||