| Article Section | |||||||||||

|

Home |

|||||||||||

Analysis of Changes in GST Invoicing System effective from 1st April, 2020 |

|||||||||||

|

|||||||||||

Analysis of Changes in GST Invoicing System effective from 1st April, 2020 |

|||||||||||

|

|||||||||||

The Invoicing System is GST is destined for major overhaul in the coming financial year. This includes E-Invoicing, Inclusion of Quick Response Code and Facility of Digital payments to recipients. It is important for organizations to understand the same as all of the above would not only require customization in their accounting/ ERP software but also require modification in the process of generation of invoice. This also has a direct implication on availment of ITC and filing of GST Returns. Let us analyse each of them basis the currently available information: 1.E- Invoicing Legal Premise: As per rule 48(4) of CGST Rules, the invoice shall be prepared by such class of registered persons as may be notified by the Government, on the recommendations of the Council, by including such particulars contained in FORM GST INV-01 after obtaining an Invoice Reference Number by uploading information contained therein on the Common Goods and Services Tax Electronic Portal in such manner and subject to such conditions and restrictions as may be specified in the notification. Therefore, the Specified Persons would be required to obtain an Invoice Reference Number (IRN) by uploading information filled in Form GST INV-01 on the common portal. As per rule 48(5) of CGST Rules, every invoice issued by a person to whom rule 48(4) applies in any manner other than the manner specified in the said sub-rule [i.e. rule 48(4)] shall not be treated as an invoice. As per rule 48(6) of CGST Rules, the provisions rule 48(1) and 48(2) shall not apply to an invoice prepared in the manner specified rule 48(4). Thus, E-invoice need not be prepared in triplicate in case of goods or duplicate in case of services. Mandatory E-invoicing if aggregate turnover exceeds ₹ 100 crores w.e.f. 01-04-2020: As per Notification No. 70/2019 – Central Tax dated 13-12-2019 with effect from 01-04-2020, the registered person, whose aggregate turnover in a financial year exceeds ₹ 100 crore rupees, as a class of registered person who shall prepare invoice in terms of rule 48(4) of the said rules in respect of supply of goods or services or both to a registered person. Notified Schema of E-Invoice vide Notification No. 02/2020 – Central Tax dated 1-01-2020: CBIC has amended CGST Rules by notifying the scheme of E-Invoice in Form INV-01. Concept of E-Invoice E-invoice does not mean generation of invoices from a central portal of tax department, as any such centralization will bring unnecessary restriction on the way trade is conducted. In fact, taxpayers have different requirements and expectation, which can’t be met from one software generating e-invoices from a portal for the whole country. It has been stated that the invoice generation interface would remain the same for the assessees (i.e. assessees can continue to generate their invoices through their existing accounting software) and they would not be required to generate any invoices on the GST portal or any other portal. However, such generated invoices will have to be uploaded at the Invoice Registration Portal (IRP) which will then generate the Invoice Reference Number (IRN) and the quick response code. The accounting software vendors would enable this aspect by way of an interface between the accounting software and the common portals and the assessee will only have to click a button to get the Invoice Reference Number (IRN) generated from the Invoice Registration Portal (IRP). Thereby, the generation of the IRN would be a faceless interface wherein the assessee will not know the process of the generation but will be given with the desired output. Generation of e-invoice will be the responsibility of the taxpayer who will be required to report the same to Invoice Registration Portal (IRP) of GST, which in turn will generate a unique Invoice Reference Number (IRN) and digitally sign the e-invoice and also generate a QR code. The QR Code will contain vital parameters of the e-invoice and return the same to the taxpayer who generated the document in first place. The IRP will also send the signed e-invoice to the recipient of the document on the email provided in the e-invoice. Type of documents to be reported to GST System As per concept paper on e-invoicing system issued by GSTN, while the word ‘invoice’ is used in the name of e-invoice, it covers other documents that will be required to be reported to IRP by the creator of the document:

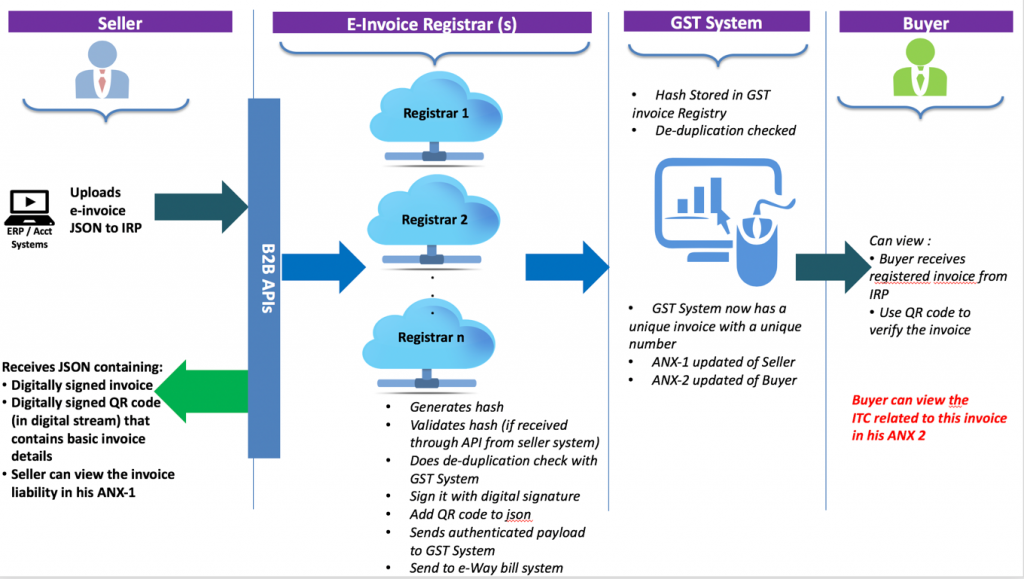

It may be noted that Rule 48 of CGST Rules deals with the manner of issue of invoice in case of supply of goods or services or both. It does not deal with issue of debit or credit notes. There has not been any corresponding change in legal provisions relating to issue of debit or credit notes with respect to issue of E-invoice. However the concept note uses the term ‘invoice’ for invoice, credit note and debit note. Furthermore, as per 2(66) of CGST Act, “invoice” or “tax invoice” means the tax invoice referred to in section 31. However the concept note refers the term E-invoice also for any other document as required by law to be reported by the creator of the document. Thus, it may be argued whether registered person supplying exempted goods may also issue E-invoice for Bill of Supply in case supply of exempted goods or services or both. There has not been any corresponding change in legal provisions concerning Bill of Supply. Thus the issue requires more clarity on the part of the Government. It looks that there is an intention that all documents generated by supplier in respect of B2B transaction must be through E-invoice. However it will require further amendment in law. Workflow of E-Invoicing The e-invoice system being implemented by tax departments across the globe consists of two important parts namely, a) Generation of invoice in a standard format so that invoice generated on one system can be read by another system. b) Reporting of e-invoice to a central system. The basic aim behind adoption of e-invoice system by tax departments is ability to pre-populate the return and to reduce the reconciliation problems. Huge increase in technology sophistication, increased penetration of Internet along with availability of computer systems at reasonable cost has made this journey possible and hence more than 60 countries are in the process of adopting the e-invoice.

The flow of the e-invoice generation, registration and receipt of confirmation can be logically divided into two major parts; PART A: The first part being the interaction between the business (supplier in case of invoice) and the Invoice Registration Portal (IRP). PART B: The second part is the interaction between the IRP and the GST/E-Way Bill Systems and the Buyer. This involves following steps; Step 1 is the generation of the invoice by the seller in his own accounting or billing system. The invoice must conform to the e-invoice schema (standards) that is published and have the mandatory parameters. The optional parameters can be according to the business need of the supplier. The supplier’s (seller’s) software should be capable to generate a JSON of the final invoice that is ready to be uploaded to the IRP. The IRP will only take JSON of the e-invoice. Step 2: This includes generation of the unique Invoice Reference Number (IRN). This is an optional step. The seller can also generate this and upload along with invoice data. The 3 parameters which will be used to generate IRN (hash) are: i. Supplier GSTIN, ii. Supplier’s invoice number and, iii. Financial year (YYYY-YY). Step 3 is to upload the JSON of the e-invoice (along with the hash, if generated) into the IRP by the seller. The JSON may be uploaded directly on the IRP or through GSPs or through third party provided Apps. Step 4: The IRP will also generate the hash and validate the hash of the uploaded json, if uploaded by the supplier. The IRP will check the hash from the Central Registry of GST System to ensure that the same invoice from the same supplier pertaining to same Fin Year is not being uploaded again. On receipt of confirmation from Central Registry, IRP will add its signature on the Invoice Data as well as a QR code to the JSON. The QR code will contain GSTIN of seller and buyer, Invoice number, invoice date, number of line items, HSN of major commodity contained in the invoice as per value, hash etc. Step 5 will involve sharing the uploaded data with GST and e-way bill system. This includes following

Step 6 will involve returning the digitally signed JSON with IRN back to the seller along with a QR code. The registered invoice will also be sent to the seller and buyer on their mail ids as provided in the invoice. Creation of E-Invoice Modes for getting invoice registered: Multiple modes will be made available so that taxpayer can use the best mode based on his/her need. The modes given below are envisaged at this stage under the proposed system for e-invoice, through the IRP (Invoice Registration Portal): a. Web based, b. API based, c. SMS based, d. mobile app based, e. offline tool based and f. GSP based. API mode: Using API mode, the big tax payers and accounting software providers can interface their systems and pull the IRN after passing the relevant invoice information in JSON format. API request will handle one invoice request at time to generate the IRN. This mode will also be used for bulk requirement (user can pass the request one after the other and get the IRN response within fraction of second) as well. The e-way bill system provides the same methodology. FAQ as provided by GSTN on E-Invoice Generic questions on e-invoice 1. Will businesses now be required to generate e-invoices on the GST portal or the e-invoice portal or the IRN portal? a. No. b. Businesses will continue to generate e-invoices on their internal systems – whether ERP or their accounting / billing systems or any other application. c. The e-invoicing mechanism only specifies the invoice schema and standard so as to be inter-operable amongst all accounting/billing software and all businesses. 2. Please clarify whether there the current e-invoice schema is for the invoice to be issued by Govt or has to be maintained in the IT system by the tax payer? a. The invoice schema has to be maintained and invoices generated using this schema by the taxpayer himself. b. The GST portal or Invoice Registration Portal (IRP) will NOT provide facility to generate invoices. IRP is only to report the invoice data. c. The ERP or accounting billing software or any other software tool to generate e-invoice of the seller shall only generate invoices. 3. Will there be separate invoice formats required for Traders, Medical Shops, Professionals and Contractors? a. No. b. Same e-invoice schema will be used by all kinds of businesses. The schema has mandatory and non-mandatory fields. Mandatory field has to be filled by all taxpayers. Non-mandatory field is for the business to choose. It covers all most all business needs and specific sectors of business may choose to use those non-mandatory field which are needed by them or their eco-system. 4. How long will the e-invoice generated would be available at the Government portal? a. It is again clarified that the e-invoice will not be generated at the GST portal. b. It will be generated only at the seller’s system – whether ERP or the accounting/billing system/other software tools of the seller. c. It will be uploaded into the GST ANX-1 only once it has been validated and registered by the invoice registration system. d. After it has been validated and is available in the ANX-1, it will be visible to the counter party in his ANX 2. e. Thereafter it will be visible and available for the entire financial year and archived. f. As far as data on IRP is concerned, it will be kept there only for 24 hours. 5. While all businesses generate invoice at the same time, how will the server react? a. The businesses will generate the invoice at their system and hence that will not impact the servers of IRP. b. The capacity of the system at IRP shall be built so as to handle the envisaged loads of simultaneous upload based on data reported in GSTR-1 for last two years. c. Subsequently, multiple invoice registrars will be made available that will be able to distribute the load for invoice registration. 6. Is it possible to auto populate fields of the e-invoice based on credentials entered? That way it can minimize data entry errors. a. Since the invoice generation is to happen at the business end, this can be built into the ERP or invoicing system of the seller. Most of such software provide this facility in the name of item master, supplier master, buyer master etc. 7. Will it be possible to add transporter details as well? a. No. b. The transporter details must be entered in the E-Way bill system only. Contents of e-invoice 1. There are certain fields today which are optional and some mandatory. How are these to be used? a. The mandatory fields are those that MUST be there for an invoice to be valid under e-Invoice Standard. b. The optional ones are those that may be needed for the specific business needs of the seller/business. These have been incorporated in the schema based on current business practices in India. c. The registration of an e-invoice will only be possible once it has ALL the mandatory fields uploaded into the Invoice registration Portal (IRP). d. A mandatory field not having any value can be reported with NIL. 2. What is the maximum Number of line items supported by e-invoice? a. The maximum number of line items per e-invoice is 100. 3. Does the e-invoice schema provide the maximum length of the various fields in the schema? a. Yes. b. Each field specification has been provided with the type of characters that are to be entered and its length as well. 4. What will be the threshold requirement for E-Invoicing applicability? a. This will be notified by the Government at the time of rollout. b. As already mentioned above, the rollout of the e-invoice mechanism will be in phases. 5. Will the e-invoice have columns to show invoice currency? a. Yes, the seller can display the currency. Default will be INR. 6. Whether the IRN is to be captured in the Supplier’s ERP? a. The IRN (hash) will be generated by GST System using GSTIN of supplier or document creator, financial year and the unique serial number of the document/invoice. The IRN can also be generated by the seller. b. The serial number of invoice will be unique for a GSTIN for a Financial Year and the same has to be captured by Supplier’s ERP. c. Supplier has to keep the IRN against each of its invoice. It will be advisable to keep the same in the ERP as invoice without IRN will not be a legal document. 7. Whether e-invoice generated is also required to be signed again by the taxpayer? a. Not mandatory. However, if a signed e-invoice is sent to IRP, the same will be accepted. b. The e-invoice will be digitally signed by the IRP after it has been validated. The signed e-invoice along with QR code will be shared with creator of document as well as the recipient. c. Once it is registered, it will not be required to be signed by anyone else. 8. Whether the facility of adding discount amount at line item-level would be mandatory in nature? a. The e-invoice has a provision for capturing discount at line item level. b. The discounting at line item level is to be mentioned only when and if it is applicable in the particular transaction. 9. Can the seller place their LOGO in the e-Invoice Template? a. There will NOT be a place holder provided in the e-invoice schema for the company logo. b. This is for the software company to provide in the billing/accounting software so that it can be printed on his invoice using his printer. However, the Logo will not be sent to IRP. In other words, it will not be part of JSON file to be uploaded on the IRP. 10. There should be a space provided for the QR code to be placed. a. The QR code will be provided to the seller once he uploads the invoice into the Invoice Registration system and the same is registered there. b. Seller can at his option may print the same on Invoice. 11. Will we be able to provide the address and bill-to party and PAN details in the e-invoice? a. Yes. b. It will be possible to provide all these details in the placeholders provided in the schema. 12. Would the Supplier be allowed to issue his own invoice and if yes, will the Invoice number and IRN be required to be mentioned? a. Yes, the supplier will issue his own system’s invoice, in the standard e-invoice schema that has been published. Invoice number is a mandatory item under GST and hence for e-invoice. b. IRN (Hash) can be provided after the e-invoice has been successfully reported to the IRP. E-Invoice will be valid only if it has IRN. 13. The current e-invoice template provides for total discount for all the products or services. Will this be possible in the e-invoice? a. Yes. b. There is a mechanism and placeholders to provide discounting on item level as well as total discounts on the invoice value. 14. Will there be an option for linking multiple invoices in case of debit note/ credit note? a. Yes, it will be allowed to link the credit/debit notes as hitherto fore. 15. Will the e-invoice schema cater to reverse charge mechanism? a. Yes. b. E-invoice system has a reverse charge mechanism reporting as well. Method of Reporting e-Invoice to GST System 1. In addition to the above, we understand that electronic invoice which will be uploaded on GST portal will be authenticated and IRN will be allocated for each e-invoices generated. a. Yes, the e-invoice will be authenticated with the digital signature of the IRP (invoice registration portal). b. IRN (Invoice Reference Number) will be the hash generated by the IRP. c. The registered invoice will be valid to be used by the business. 2. Will it be possible for bulk uploading of invoices for e-invoicing as well? a. Invoices have to be uploaded on IRP one at a time. b. The IRP will be able to handle a large sequence of invoices for registration and validate them. Essentially bulk upload will be required by large taxpayers who generate large number of invoices. Their ERP or accounting system will have to be designed in such a way that it makes request one by one. For the user, it will not make any difference. 3. Will the requirement for such invoices to be authenticated by the supplier using a digital signature/signature be done away with? a. The seller will need to upload the e-invoice into the Invoice Registration Portal. b. The signing of e-invoice by seller is not mandatory. 4. Will there be a time limit for e-invoice uploading for registration? a. Yes, that will be notified by the Government. Without registration of e-invoice the same will not be valid. Required changes will be made in the law. b. Once uploaded to the invoice registration portal (IRP), it will be registered immediately, on real-time basis. 5. Will it be possible to allow invoices that are registered on invoice registration system/portal to be downloaded and/or saved on handheld devices? a. Yes. b. IRP System after registering the invoice, will share back digitally signed e-invoice for record of supplier. It will also be sent to the email address of recipient provided in the e-invoice. 6. Will it be possible to print the e-invoice? a. Yes. b. It will be possible for both the seller as well as the buyer to print the invoice, using the QR code as well as signed e-invoice returned by the Invoice Registration Portal (IRP). Amendment/cancellation of e-invoice 1. Whether e-invoices generated through GST system can be partially/fully cancelled? a. E-Invoice can’t be partially cancelled. It has to be fully cancelled. b. The e-invoice mechanism enables invoices to be cancelled. This will have to be reported to IRN within 24 hours. Any cancellation after 24hrs could not be possible on IRN, however one can manually cancel the same on GST portal before filing the returns. 2. How would amendments be allowed in e-invoice? a. Amendments to the e-invoice are allowed on GST portal as per provisions of GST law. All amendments to the e-invoice will be done on GST portal only. Relationship with e-way bill 1. With the introduction of e-invoices, what are the documents need to be carried during transit of goods? a. For transportation of goods, the e-way bill will continue to be mandatory, based on invoice value guidelines, as hitherto fore. This aspect will be notified by the Government when this mechanism will be notified. Export/Import 1. Please clarify whether exports would require e-invoice compliance. a. Yes. b. The e-invoice schema also caters to the export invoices as well. The e-invoice schema is based on most common standard, this will help buyer’s system to read the e-invoice. 2. Does the e-invoice allow the declaration of export invoices/ zero rated supplies? a. Yes. b. It allows the declaration of export invoices / zero rated supplies. Others 1. What will be the workflow of the end to end e-invoice mechanism? a. The end to end workflow will be provided by at the time of rollout of the e-invoice system. 2. Will the industry be provided sufficient time for preparation? a. Yes. b. The e-invoice mechanism is expected to be rolled out in phases from 01st Jan 2020 on voluntary basis. c. Initially, the e-invoice mechanism will be allowed for tax payers above a certain turnover or above a certain invoice value or also to volunteers. d. Subsequently, it will be enabled for all tax payers in a phased step-wise manner. e. Details of these will be published subsequently. 2. Quick Response Code- QR Code Legal Premise As per sixth proviso to Rule 46 of the CGST Rules, the Government may, by notification, on the recommendations of the Council, and subject to such conditions and restrictions as mentioned therein, specify that the tax invoice shall have Quick Response (QR) code. The CBIC had issued Notification No. 72/2019 – Central Tax dated 13-12-2019 in this regard. As per the Notification with effect from 01-04-2020, an invoice issued by a registered person, whose aggregate turnover in a financial year exceeds INR 500 Cr, to an unregistered person (hereinafter referred to as B2C invoice), shall have Quick Response (QR) code. Further, where such registered person makes a Dynamic Quick Response (QR) code available to the recipient through a digital display, such B2C invoice issued by such registered person containing cross-reference of the payment using a Dynamic Quick Response (QR) code, shall be deemed to be having Quick Response (QR) code. Thus, QR Code will be mandatory for companies having aggregate turnover above INR 500 cr for all B2C Supplies. This includes supplies to employees including Canteen and other recoveries. 3.Facility of digital payment to Recipient The section 31A has been inserted vide Finance (No. 2) Act,2019 w.e.f. 01-01-2020. As per section 31A, the Government may, on the recommendations of the Council, prescribe a class of registered persons who shall provide prescribed modes of electronic payment to the recipient of supply of goods or services or both made by him and give option to such recipient to make payment accordingly, in such manner and subject to such conditions and restrictions, as may be prescribed. Author’s Recommendation It is recommended that all the corporates having aggregate turnover more than INR 100 cr may gear up their systems to enable E-invoicing along with QR Code. This will become mandatory for all B2B transactions from 1st April, 2020. Thus, the invoice will be valid invoice only when it has Invoice reference number mentioned in it. Since the data of E-invoice will be used to generate Part A of E-way bill, it is important that the invoicing systems of the entities may be fully customized to manage the workload at all times. The government has notified multiple Invoice registration portals (IRPs) to facilitate and manage the workload. However, their exact performance will be gauged only when the system is up and running. Since this data is directly feeding GST ANX-1 (Statement of Outward Supplies) of seller and GST ANX-2 (Virtual Purchase register or GSTR-2A) of buyer, it will aid in reconciliation of both. The operational issue which will be faced by the entities that E-invoice cannot be cancelled post 24 hours of their generation. Thus, in case any invoice requires cancellation or amendment, it can only be done through raising a debit or credit note. From the department’s point of view, this may greatly minimize the issue of Fake invoicing which is one of the core concerns of the government. Similarly the provision of QR code and facility of Digital payments for B2C payments may bring great efficiency for Retail and E-commerce companies.

By: Chitresh Gupta - January 9, 2020

Discussions to this article

I don't see any reason why GST authorities should get into this mess of E-Invoice. Unfortunately there is no proper infrastructure to encourage this new concept of E-Invoice and lack of preparedness of Trade & Industry to upgrade to this technology. Department has Notified 10 website vide Notification.69/2019 and none of them are functional yet. There are plethora of operational issues which none have foreseen for this new concept. For instance a simple Data entry mistake, there is no option for amendment once Invoice is registered on IRP other than to cancel such invoice. Calling back information once sent across to the recipient on the registered email is another nuance. Before even Assessee have been migrated to new returns this new technology is a hasty decision of Government authorities. Lot of Tax Payer's money is going to drain in the name of technology upgradation.

I think it is very important to plug the leakages. e-invoicing system will be of great help. The same system is operating in more than 60 countries successfully. We must control leakages for better society. Any new system take times to established. As GSTN is established, the same will also.

Controlling leakage under GST is a good motive. But how can it be achieved, was it demonstrated or explored with realistic examples. What great difference can authorities bring in, when we have been filing GSTR-1. 60 Nations have already brought in this model. What is their status of stability post implementation of so-called GST in their nation. What is the concept of GST they have adopted and what is the preparedness of the nation to adopt the concept of E-Invoice. Is it a responsibility of authorities under Information Technology Act or GST or ICAI to think of brining a change in the Economy for the concept called E-Invoice. GSTN is not yet settled, it is still settling down. Migration to new mechanism of GST Returns has not been commenced and we are talking about a model which is unseen in India thoroughly. Were there realistic test models of 10 entities picked up (both Rural & Urban) for usage of E-Invoice before making a law in this regard is a question Tax Administration authorities have to think of.

|

|||||||||||

| |

|||||||||||