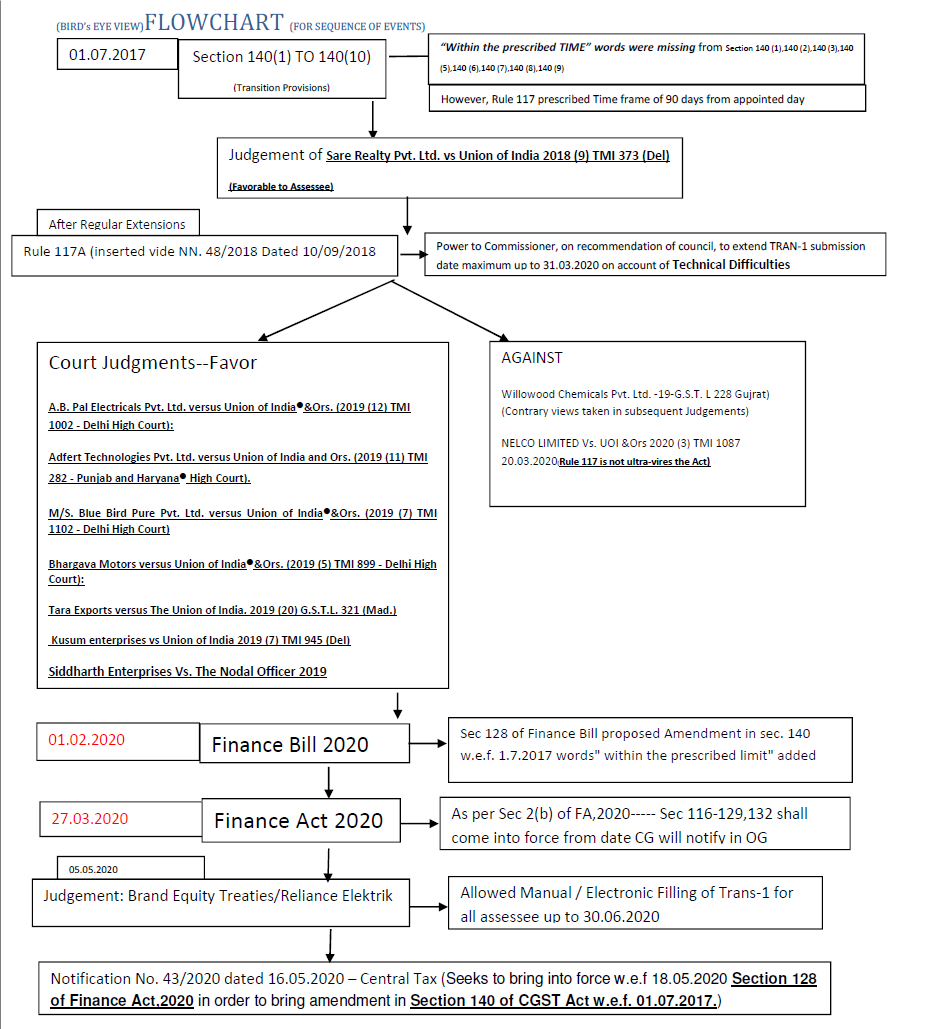

ANALYSIS OF ABOVE EVENTS:

1) Analysis of Judgement of BRAND EQUITY TREATIES LIMITED, MICROMAX INFORMATICS LTD., DEVELOPER GROUP INDIA PRIVATE LIMITED, RELIANCE ELEKTRIK WORKS VERSUS THE UNION OF INDIA AND ORS.[ 2020 (5) TMI 171 - DELHI HIGH COURT] (Delhi HC-Writ Pronounced on 05.05.2020)

(5 applicants seek the identical relief for identical controversy)

1.1 Relief: -

- To permit the petitioners to avail ITC of accumulated CENVAT credit by filling Trans 1 beyond time prescribed in Rules.

- Rule 117 is arbitrary, unconstitutional & violative of Article 14(Equality before Law) to the extent it proposes time limit for c/f of CENVAT Credit to GST regime.

1.2 Facts:- There has been delay in filling of Form Trans 1 and factual situation in each one of present case is different and is substantially distinguishable from cases where relief already granted on the ground that the delay was not on account of Technical glitch on the portal, but due to technical difficulties at the end of assessee.

The case relates only to the Transitional Credit u/s 140(1) i.e. Credit as per Return immediately filed before appointed date.

1.3 Arguments forwarded by Assessee: -

- CENVAT Credit accumulated in erstwhile regime represents the property of petitioner which is vested Right and cannot be taken away on failure to fulfill conditions procedural in nature. It is a constitutionally protected right.

- Time limit in Rule 117 is procedural in nature and not mandatory, as it is without substantive provision.

1.4 Arguments of the Department: -

- Delay is due to casual approach & negligence, not attributable to any technical glitch.

- Defended Rule 117 by referring to section 164 of CGST Act.

- "in such manner as may be prescribed" in section 140(1) empowers Govt. to fix time frame.

- ITC is a benefit/ concession extended as per scheme of the statute subject to certain conditions and is not a vested right.

1.5 Held:-(It can be classified under 3 broad heads)

a) TIME PERIOD UNDER RULE 117

- Time period for furnishing Trans 1 has been extended from time to time by Govt. Acknowledging the technical difficulties faced by the taxpayers owing to several judgments and committee reports and finally 117A was inserted vide Notification 48/2018 inserted to empower commissioner , on recommendation of council, to extend TRAN-1 submission date maximum up to 31.03.2020 on account of Technical Difficulties

- This also substantiates that the period for filing the TRAN-1 is not considered – either by the legislature, or the executive as sacrosanct or mandatory and is extended from time to time, largely on account of its inefficient network.

- The Act does not completely restrict the transition of CENVAT credit in the GST regime by a particular date, and there is no rationale for curtailing the said period, except under the law of limitations.

- Taxpayers cannot be robbed of their valuable rights on an unreasonable and unfounded basis of them not having filed TRAN-1 Form within 90 days, when civil rights can be enforced within a period of three years from the date of commencement of limitation under the Limitation Act, 1963.

- Section 140 (1) is categorical. It states only the manner i.e. the procedure of carrying forward was left to be provided by use of the words “in such manner as may be prescribed”.

- In absence of any consequence being provided under Section 140, to the delayed filing of TRAN-1 Form, Rule 117 has to be read and understood as directory and not mandatory. The procedure could not run contrary to the substantive right vested Section 140(1).

- However, it does not mean that the availing of CENVAT credit can be in perpetuity. In absence of any specific provisions under the Act, we would have to hold that in terms of the residuary provisions of the Limitation Act, the period of three years should be the guiding principle and thus a period of three years from the appointed date would be the maximum period for availing of such credit.

b) CENVAT CREDIT IS A VESTED RIGHT

- The credit of taxes already paid in every sense stood accumulated, acquired and vested on the appointed date as it was reflected in the said CENVAT credit register in the previous regime.

- The CENVAT credit which stood accrued and vested is the property of the assessee, and is a constitutional right under Article 300A of the Constitution. The same cannot be taken away merely by way of delegated legislation by framing rules, without there being any overarching provision in the GST Act.

- This credit, under the Section 140(1), has to be carried forward and in that sense, the vested right of the property of the petitioner stood accrued and the same cannot be taken away by the respondents by way of Rules.

c) TECHNICAL DIFFICULTY (A broad definition)

- "Technical difficulty on the common portal” imply? There is no definition to this concept and the respondent seems to contend that it should be restricted only to “technical glitches on the common portal”. However, “Technical difficulty” is too broad a term and cannot have a narrow interpretation, or application. Further, technical difficulties cannot be restricted only to a difficulty faced by or on the part of the respondent. It would include within its purview any such technical difficulties faced by the taxpayers as well, which could also be a result of the respondent’s follies. Thus, the phrase “technical difficulty” is being given a restrictive meaning which is supplied by the GST system logs.

- There could be various different types of technical difficulties occurring on the common portal which may not be solely on account of the failure to upload the form. The access to the GST portal could be hindered for myriad reasons, sometimes not resulting in the creation of a GST log-in record. Further, the difficulties may also be offline, as a result of several other restrictive factors. It would be an erroneous approach to attach undue importance to the concept of “technical glitch” only to that which occurs on the GST Common portal, as a pre- condition, for an assessee/taxpayer to be granted the benefit of Sub- Rule (1A) of Rule 117.It cannot be arbitrary or discriminatory, if it has to pass the muster of Article 14 of the Constitution.

1.6 IMPACT

Permitted to file relevant TRAN-1 Form on or before 30.06.2020. Respondents are directed to either open the online portal so as to enable the Petitioners to file declaration TRAN-1 electronically, or to accept the same manually. Respondents shall thereafter process the claims in accordance with law. We are also of the opinion that other taxpayers who are similarly situated should also be entitled to avail the benefit of this judgment.

The other decisions as referred above for allowing transitional credits are discussed as follows:

The other side of the coin as referred above, the judgements Against allowing belated transitional credits are discussed as follows:

2 Amendment in Section 140 by Finance Act, 2020

|

Section

Amended

|

Old Provision

|

Amendment

|

New Provision

|

Reason

|

Effect

|

|

Section 140 (1),

Section 140 (2),

Section 140 (3),

Section 140 (5),

Section 140 (6),

Section 140 (7),

Section 140 (8),

Section 140 (9)

(Transitional

Credit Provisions)

|

140. (1) A registered person, other than a person opting to pay tax under section 10, shall be entitled to take, in his electronic credit ledger, the amount of CENVAT credit carried forward in the return relating to the period ending with the day immediately preceding the appointed day, furnished by him under the existing law in such manner as may be prescribed:

………

(2) A registered person, other than a person opting to pay tax under section 10, shall be entitled to take, in his electronic credit ledger, credit of the unavailed CENVAT credit in respect of capital goods, not carried forward in a return, furnished under the existing law by him, for the period

ending with the day immediately preceding the appointed day in such manner as may be prescribed:

|

(1), after the words “existing law”, the words “within such time and” shall be inserted and shall be deemed to have been inserted;

(2), after the words “appointed day”, the words “within such time and” shall be inserted and shall be deemed to have been inserted;

(3), for the words “goods held in stock on the appointed day subject to”, the words “goods held in stock on the appointed day, within such time and in such manner as may be prescribed, subject to” shall be substituted and shall be deemed to have been substituted;

(5), for the words “existing law”, the words “existing law, within such time and in such manner as may be prescribed” shall be substituted and shall be deemed to have been substituted;

(6), for the words “goods held in stock on the appointed day subject to”, the words “goods held in stock on the appointed day, within such time and in such manner as may be prescribed, subject to” shall be substituted and shall be deemed to have been substituted;

(7), for the words “credit under this Act even if”, the words “credit under this Act, within such time and in such manner as may be prescribed, even if” shall be substituted and shall be deemed to have been substituted;

(8), for the words “in such manner”, the words “within such time and in such manner” shall be substituted and shall be deemed to have been substituted;

(9), for the words “credit can be reclaimed subject to”, the words “credit can be reclaimed within such time and in such manner as may be prescribed, subject to” shall be substituted and shall be deemed to have been substituted.

|

(1) A registered person, other than a person opting to pay tax under section 10, shall be entitled to take, in his electronic credit ledger, the amount of CENVAT credit carried forward in the return relating to the period ending with the day immediately preceding the appointed day, furnished by him under the existing law within such time and in such manner as may be prescribed:

………………………….

(2) A registered person, other than a person opting to pay tax under section 10, shall be entitled to take, in his electronic credit ledger, credit of the unavailed CENVAT credit in respect of capital goods, not carried forward in a return, furnished under the existing law by him, for the period ending with the day immediately preceding the appointed day within such time and in such manner as may be prescribed:

…………………………………..

|

Section 140 of the CGST Act is being amended w.e.f. 01.07.17, to prescribe the manner and time limit for taking transitional credit

|

Retrospective

Amendment w.e.f

01.07.2017 to

overcome the

effect of

Judgements like

Siddhartha

Enterprises etc.

allowing

Transitional Credit

based upon the

ground that Rules

cannot provide the

Time Limit when in

Act, there is No

Time Frame

Provided.

Procedural

amendment in Act

in Sections 140(1),

(2), (3), (5), (6), (7),

(8), (9) to include

provision for Time

Frame for

Transitional Credit

to be provided by

Rules.

This may imply that

the ground raised

by the petitioner

before various

courts challenging

vires of Rule 117 of

the CGST Act, 2017

stands exhausted.

|

3 “A retrospective googly” Notification No. 43/2020- Central Tax dated 16.05.2020- - has enforced the retrospective amendment made in section 140 of the CGST Act vide section 128 of the Finance Act, 2020 as per section 1(2) of Finance Act, 2020. The opening lines of section 128 states that the same is effective from 1st July, 2017. However, the same has been notified vide Notification No. 43/2020-Central Tax dated 16th May, 2020, which stipulates that the said provision shall come into force on 18th May, 2020. In the author’s opinion it is applicable retrospectively from 01.07.2017.

4 Can Government bring retrospective Amendments

The power of the government to make retrospective law cannot be denied but however is a limited power. The legislature cannot set at naught the judgements pronounced and overturn these by amending laws not for purpose of making corrections or removing anomalies but to bring in new provisions which did not exist earlier. The mute question is whether Statutes dealing with Substantive/Vested Rights can be retrospectively amended.

|

Citation

|

Case Law

|

|

THE STATE OF KARNATAKA & ORS. VERSUS THE KARNATAKA PAWN BROKERS ASSN. & ORS. [2018 (3) TMI 1064 - SUPREME COURT]

|

Legislative, power of (Retrospective amendment) - Whether Legislature has power to enact validating laws even with retrospective effect, however, this can be done to remove causes of invalidity - Held, yes - Whether thus, Legislature cannot set at naught judgments which have been pronounced by amending law not for purpose of making corrections or removing anomalies but to bring in new provisions which did not exist earlier - Held, yes - Whether a judicial pronouncement is always binding unless, very fundamentals on which it is based are altered and decision could not have been given in altered circumstances - Held, yes - Whether Legislature cannot, by way of introducing an amendment, overturn a judicial pronouncement and declare it to be wrong or a nullity - Held, yes - Whether what Legislature can do is to amend provisions of statute to remove basis of judgment - Held, yes [Paras 22 and 23]

|

|

Hitendra Vishnu Thakur vs. State of Maharashtra [1994 (7) TMI 343 - SUPREME COURT]

|

A procedural statute should not generally speaking be applied retrospectively where the result would be to create new disabilities or obligations or to impose new duties in respect of transactions already accomplished.

|

|

CHEVITI VENKANNA YADAV VERSUS STATE OF TELANGANA AND ORS. [2016 (10) TMI 1229 - SUPREME COURT]

|

Whether the base of earlier judgment has been removed to erase the effect of the judgment? - Held that: - The legislature cannot, by way of an enactment, declare a decision of the court as erroneous or a nullity, but can amend the statute or the provision so as to make it applicable to the past. The legislature has the power to rectify, through an amendment, a defect in law noticed in the enactment and even highlighted in the decision of the court. This plenary power to bring the statute in conformity with the legislative intent and correct the flaw pointed out by the court, can have a curative and neutralizing effect. When such a correction is made, the purpose behind the same is not to overrule the decision of the court or encroach upon the judicial turf, but simply enact a fresh law with retrospective effect to alter the foundation and meaning of the legislation and to remove the base on which the judgment is founded. This does not amount to statutory overruling by the legislature. In this manner, the earlier decision of the court becomes non-existent and unenforceable for interpretation of the new legislation. No doubt, the new legislation can be tested and challenged on its own merits and on the question whether the legislature possesses the competence to legislate on the subject matter in question, but not on the ground of over-reach or colorable legislation.

|

|

THE COMMISSIONER OF INCOME TAX-XVI VERSUS KARAN BIHARI THAPAR [2010 (9) TMI 160 - DELHI HIGH COURT]

|

Amendment brought being substantive in nature, cannot be given retrospective effect.

|

However, there are judgements favoring Retrospective Amendments like RC. TOBACCO PVT. LTD. VERSUS UNION OF INDIA [2005 (9) TMI 80 - SUPREME COURT], ASSISTANT COMMISSIONER OF AGRICULTURAL INCOME TAX & ORS. VERSUS M/S. NETLEY 'B' ESTATE & ORS. [2015 (3) TMI 723 - SUPREME COURT]

5 IMPLICATIONS:

1) At first Instance, the said notification negates the effect of all such orders to the extent of validity of time period provisions, as prescribed in Rule 117.The legal loophole has been plugged by the government and it will surely open up another round of litigation in this regard.

2) However, the Hon’ble HC in case of Brand Equities has given a wider definition of Technical Difficulties, hence the assessee can take the benefit of Rule 117A in which the time period has been extended to 31.03.2020 and till 30.06.2020 due to covid Blanket exemption vide Not. 35/2020, based upon the reasonable ground of technical difficulties.

3) Moreover, the sufficiency of time period prescribed of 90 days plus 90 days extension as per Rule 117(1) can also be made a point to ponder, that the same is insufficient or inappropriate for transitional credit involving number of issues, as against the preparedness of the government in implementation of GST procedures involving number of technical glitches.

4) As per the judgements quoted above the Hon’ble courts have held that the credit as reflecting in earlier regime returns is a VESTED Right in pursuance of Article 300A of constitution and if it is a vested right, it cannot be curtailed. It must be appreciated that the credit being sought, may be belated, but belongs to the credit of taxes already paid by the registered person. Even the Gujrat HC in case of Shabnam Petro Fills Pvt. Ltd., though on different issue but has considered ITC a vested Right.

Even the Hon’ble SC in Eicher Motors Ltd. V. UOI 1999 (1) TMI 34 - SUPREME COURT , COLLECTOR OF CENTRAL EXCISE, PUNE VERSUS DAI ICHI KARKARIA LTD. 1999 (8) TMI 920 - SUPREME COURT , Samtel India Ltd. v/s CCE, Jaipur 2003 (3) TMI 121 - SUPREME COURT, Jayam and Co. v/s Assistant Commissioner 2016 (9) TMI 408 - SUPREME COURT , New Swadeshi Sugar Mills (2016) 1 SCC 614, Osram Surya (P) Ltd. V Commissioner of Central Excise, Indore 2002 (5) TMI 49 - SUPREME COURT has held ITC a vested Right.

Although, on the other side of the coin, Bombay High Court has held, the same is taken as a mere concession given by Statute and not a right.

5) As ITC is the vested right and curtailing it through Retrospective Amendment, the validity of bringing in Retrospective amendment by Government can be challenged. It is a Procedural Amendment Affecting Vested Substantive Right of a Litigant. How a vested right can be taken away by a retrospective law amendment.

6 RECOMMENDATION:

- Hence, it shall be open to the registered person to claim its credits on various other grounds as mentioned above. As a matter of abundant caution, all such claims should be filed before 30.06.2020(before expiry of Limitation period),online, if the jurisdictional officer allows or manually to the jurisdictional officer to keep the claim alive in light of the judgement in due course and maintaining the trail keeping in mind the judgement of M/s Shree Motors Vs. UOI [2020 (3) TMI 728 - RAJASTHAN HIGH COURT]The registered person can also seek to Legal Remedy by filling a Writ. Despite all, the fact is that, still there are a number of questions that are unanswered like jurisdictional restrictions of High Court decision, validity of Retrospective Amendment, preparedness of GSTN, extensions pertaining to arbitrary approach of Government and will be settled in due course by the Hon’ble courts.

By: AANCHAL KAPOOR -

June 8, 2020

Discussions to this article

Madam,

CBIC has taken Draconian steps by retrospective amendments in S.140, w.e.f. 1.7.2017, so as to nullify all the favourable judgments of different courts and determined to reject the genuine claims of the assessees. Such type of steps on the part of the GOVT agency are indeed non judicious. The GOVT agency has ample public money to waste on legal matters to harass the public, but what a common man will do in such a situation in view of the different judgments of Apex court as under;

The Supreme Court has also held that the taxing statutes are to be interpreted literally : The State of Karnataka v. M.K. Agro Tech Pvt. Ltd. 2017 (9) TMI 1308 - SUPREME COURT, Commissioner of Customs v. Dilip Kumar and Company 2018 (7) TMI 1826 - SUPREME COURT, Eureka Forbes Limited v. State of Bihar and Ors. 2014 (7) TMI 235 - SUPREME COURT

It has also been held by the Supreme Court that the court only interprets the law within the four corners of the Act and cannot legislate it under the disguise of interpretation. In case a provision of law is misused and subjected to the abuse of process of law, it is for the legislature to amend, modify or repeal : Vemareddy Kumaraswamy Reddy v. State of A.P. 2006 (2) TMI 640 - SUPREME COURT.

Moreover, it has been observed in the past, that every time, the fair judgments of various courts in GST are being turned down by CBIC, by bringing amendments in Act and/or rules, by harassing the public at large and no one is there to stop Draconian steps of CBIC.

Common man is not having enough time & money to carry on the legal battle for a long time as the Govt has.

Sir! I do understand your point of mentioning Wastage of Resources and Time on the part of Assessee that to due to mistake of other. The defects in legislation are being borne by the Registered Persons. Now, let's see how this retrospective amendement stands in due course of time, it will decide the fate of Trans 1 credit eligibility.

|