| Article Section | |||||||||||||||||||||

INCOME DEEMED TO ACCRUE/ARISE IN INDIA FOR NON-RESIDENT |

|||||||||||||||||||||

|

|||||||||||||||||||||

INCOME DEEMED TO ACCRUE/ARISE IN INDIA FOR NON-RESIDENT |

|||||||||||||||||||||

|

|||||||||||||||||||||

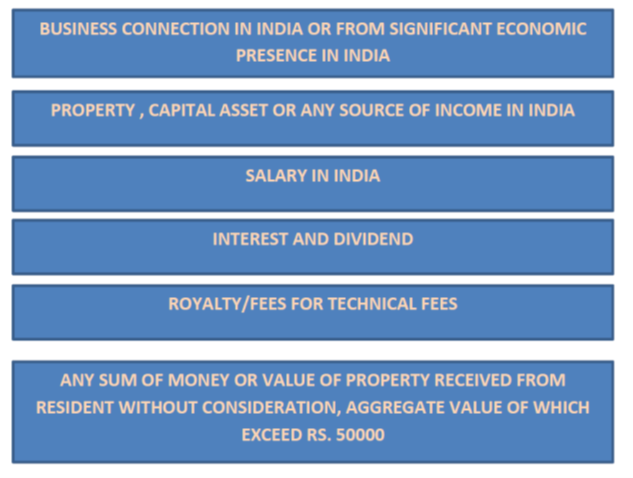

INCOME DEEMED TO ACCRUE/ARISE IN INDIA IN THE HANDS OF NON-RESIDENT (SEC 9 OF THE INCOME TAX ACT) This area is a complicated one which needs to be understood wisely and carefully while calculating the Total Taxable income of Non-resident. INCOME ACCRUING OR ARISING FROM

Further, Income arising to the Non-resident by way of :

Shall be taxable irrespective of

Business connection includes a profession at connection. Business connection includes any activity carried out through a person acting on behalf of a non-resident who performs any one or more of the following:

(i) in the name of the non-resident; or (ii) for the transfer of the ownership of, or for the granting of the right to use, property owned by that non-resident or that non-resident has the right to use; or (iii) for the provision of services by the non-resident; or

Exclusion

Significant Economic Presence-shall constitute business connection in India and shall mean— (a) transaction in respect of any goods, services or property carried out by a non-resident with any person in India including provision of download of data or software in India, if the aggregate of payments arising from such transaction or transactions during the previous year exceeds Rs. 2 crore as may be prescribed; or (Rule 11UD) (b) systematic and continuous soliciting of business activities or engaging in interaction with 3 lakh number of users in India, as may be prescribed. (Rule 11UD ) Provided that the transactions or activities shall constitute significant economic presence in India, whether or not— (i) the agreement for such transactions or activities is entered in India; or (ii) the non-resident has a residence or place of business in India; or (iii) the non-resident renders services in India: Provided further that only so much of income as is attributable to the transactions or activities referred to in clause (a) or clause (b) shall be deemed to accrue or arise in India. Taxability of Income from Business connection/Significant economic presence- Following income shall be taxable in the hands of Non-resident in such forms and manner as prescribed: (i) In the case of business where all the operations are not carried out in India , under this only such part of business income which is reasonably attributable to the operations carried out in India will be considered as deemed to accrue/arise in India. (ii) Business income generated from the business activity carried out by any person on behalf of Non-resident, only such part of business income which is reasonably attributable to the operations carried out in India will be considered as deemed to accrue/arise in India. (iii) Income from such advertisement which targets a customer who resides in India or a customer who accesses the advertisement through internet protocol address located in India; (iv) Income from the sale of data collected from a person who resides in India or from a person who uses internet protocol address located in India; (v) Income from sale of goods or services using data collected from a person who resides in India or from a person who uses internet protocol address located in India. (vi) Income from transaction in respect of any goods, services or property carried out by a non-resident with any person in India including provision of download of data or software in India, if the aggregate of payments arising from such transaction or transactions during the previous year exceeds Rs. 2 crore. (vii) Income from systematic and continuous soliciting of business activities or engaging in interaction with 3 laks number of users in India. (viii) Where any person acting on behalf of Non-resident, conclude any contract or habitually maintains stock of goods or merchandise from which he regularly delivers goods or merchandise or habitually secures orders in India mainly or wholly for the non-resident or for the other non-resident under the same management and control, then only so much of income as is attributable to the operations carried out in India shall be deemed to accrue or arise in India. Exclusion- In the case of a non-resident, no income shall be deemed to accrue or arise in India to him through or from : (i) Operations which are confined to the purchase of goods in India for the purpose of export. (ii) Person engaged in the business of running a news agency or of publishing newspapers, magazines or journals, no income shall be deemed to accrue or arise in India to him through or from activities which are confined to the collection of news and views in India for transmission out of India ; (iii) In the case of a non-resident, being— (1) an individual who is not a citizen of India ; or (2) a firm which does not have any partner who is a citizen of India or who is resident in India ; or (3) a company which does not have any shareholder who is a citizen of India or who is resident in India, no income shall be deemed to accrue or arise in India to such individual, firm or company through or from operations which are confined to the shooting of any cinematograph film in India; (iv) In the case of a foreign company engaged in the business of mining of diamonds, no income shall be deemed to accrue or arise in India to it through or from the activities which are confined to the display of uncut and unassorted diamond in any special zone notified by the Central Government in the Official Gazette in this behalf.

(a) all income accruing or arising, whether directly or indirectly, through or from any property in India, or through or from any asset or source of income in India, or through the transfer of a capital asset situated in India. ( "through" shall mean and include and shall be deemed to have always meant and included "by means of", "in consequence of" or "by reason of".) (b) an asset or a capital asset being any share or interest in a company or entity registered or incorporated outside India shall be deemed to be and shall always be deemed to have been situated in India, if the share or interest derives, directly or indirectly, its value substantially from the assets located in India. Further the share or interest, shall be deemed to derive its value substantially from the assets (whether tangible or intangible) located in India, if, on the specified date,

(the value of an asset shall be the fair market value as on the specified date, of such asset without reduction of liabilities, if any, in respect of the asset, determined in such manner as may be prescribed) Exclude- Income deemed to accrue/arise in India shall not include following: (a) It shall not apply to an asset or capital asset, which is held by a non-resident by way of investment, directly or indirectly, in a Foreign Institutional Investor as referred to in clause (a) of the Explanation to section 115AD, i.e. where income in respect of such units is taxable @ 20% in case of FII or @ 10% in case of specified fund, subject to deduction of tax @ 5% u/s 194LD. (b) It shall not apply to an asset or capital asset, which is held by a non-resident by way of investment, directly or indirectly, in Category-I or Category-II foreign portfolio investor under the Securities and Exchange Board of India. (c) It shall not apply to an asset or a capital asset, which is held by a non-resident by way of investment, directly or indirectly, in Category-I foreign portfolio investor under the Securities and Exchange Board of India (Foreign Portfolio Investors) Regulations, 2019, made under the Securities and Exchange Board of India Act, 1992.

Income under the head “Salary” shall be deemed to be income earned in India if, it is payable for:

It shall be taxable irrespective of the place of receipt of salary or the residential status. Salary income paid by Government to a citizen of India, such as diplomats, for services rendered outside India would also become taxable in India. All components of salary including allowances, perquisites and non-cash benefits are taxable unless specifically exempted.

Dividend- Dividend usually refers to the distribution of profits by a company to its shareholders. However, in view of Section 2(22) of the Income-tax Act, the dividend shall also include the following: (a) Distribution of accumulated profits to shareholders entailing release of the company's assets; (b) Distribution of debentures or deposit certificates to shareholders out of the accumulated profits of the company and issue of bonus shares to preference shareholders out of accumulated profits; (c) Distribution made to shareholders of the company on its liquidation out of accumulated profits; (d) Distribution to shareholders out of accumulated profits on the reduction of capital by the company; and (e) Loan or advance made by a closely held company to its shareholder out of accumulated profits. Dividend received from investment made in shares of Indian company or units of Mutual fund in India shall be taxable in the hands of Non-resident. Interest- Interest income received by a non-resident from

Where interest is payable in respect of any debt incurred, or moneys borrowed and used, for the purposes of a business or profession carried on by such person in India.

(Permanent establishment in India includes a fixed place of business through which the business of the enterprise is wholly or partly carried on)

Royalty- "Royalty" means consideration (including any lump sum consideration) (but excluding any consideration which would be the income of the recipient chargeable under the head "Capital gains") for— (i) the transfer of all or any rights (including the granting of a licence) in respect of a patent, invention, model, design, secret formula or process or trade mark or similar property ; (ii) the imparting of any information concerning the working of, or the use of, a patent, invention, model, design, secret formula or process or trade mark or similar property ; (iii) the use of any patent, invention, model, design, secret formula or process or trade mark or similar property ; (iv) the imparting of any information concerning technical, industrial, commercial or scientific knowledge, experience or skill (iva) the use or right to use any industrial, commercial or scientific equipment but not including the amounts referred to in section 44BB; (v) the transfer of all or any rights (including the granting of a licence) in respect of any copyright, literary, artistic or scientific work including films or video tapes for use in connection with television or tapes for use in connection with radio broadcasting ; or (vi) the rendering of any services in connection with the activities referred to in sub-clauses (i) to (iv), (iva) and (v). Inclusion.— (i) That the transfer of all or any rights in respect of any right, property or information includes and has always included transfer of all or any right for use or right to use a computer software (including granting of a licence) irrespective of the medium through which such right is transferred. (ii) That the royalty includes and has always included consideration in respect of any right, property or information, whether or not— (a) the possession or control of such right, property or information is with the payer; (b) such right, property or information is used directly by the payer; (c) the location of such right, property or information is in India. Taxability of Royalty- Income by way of Royalty shall be taxable-

Exclusion- Income by way of Royalty for the following shall not be taxable- Royalty as consists of lump sum payment made by a person, who is a resident, for the transfer of all or any rights (including the granting of a licence) in respect of computer software supplied by a non-resident manufacturer along with a computer or computer-based equipment under any scheme approved under the Policy on Computer Software Export, Software Development and Training, 1986 of the Government of India. Fees for Technical services Fees for technical services" means any consideration (including any lump sum consideration) for the rendering of any managerial, technical or consultancy services (including the provision of services of technical or other personnel) but does not include consideration for any construction, assembly, mining or like project undertaken by the recipient or consideration which would be income of the recipient chargeable under the head "Salaries"; Taxability of Fees for technical services It shall be taxable if,

Clause (viii) to sub section (1) of Section 9 of the Act provides that where any non-resident received from the resident person,

SUMMARIZED TABLE FOR TAXABILITY OF NON-RESIDENT

By: GEETANJALI PANDEY - April 29, 2023

|

|||||||||||||||||||||

| |

|||||||||||||||||||||